Summary

Klaviyo Stock Not Available: Why DTC Brands Should Care

Klaviyo isn't publicly traded. You can't buy shares anywhere as of May 2026. The company pulled its IPO filing in 2023 and stayed private which means regular investors are locked out.

This catches a lot of DTC brands off guard. September 2023 had genuine IPO buzz. If you're wondering whether this matters for platform evaluation or investment exposure, here's the situation: why they pulled back, what the valuation looks like now, and whether secondary markets are even a real option.

Why There's No Klaviyo Stock

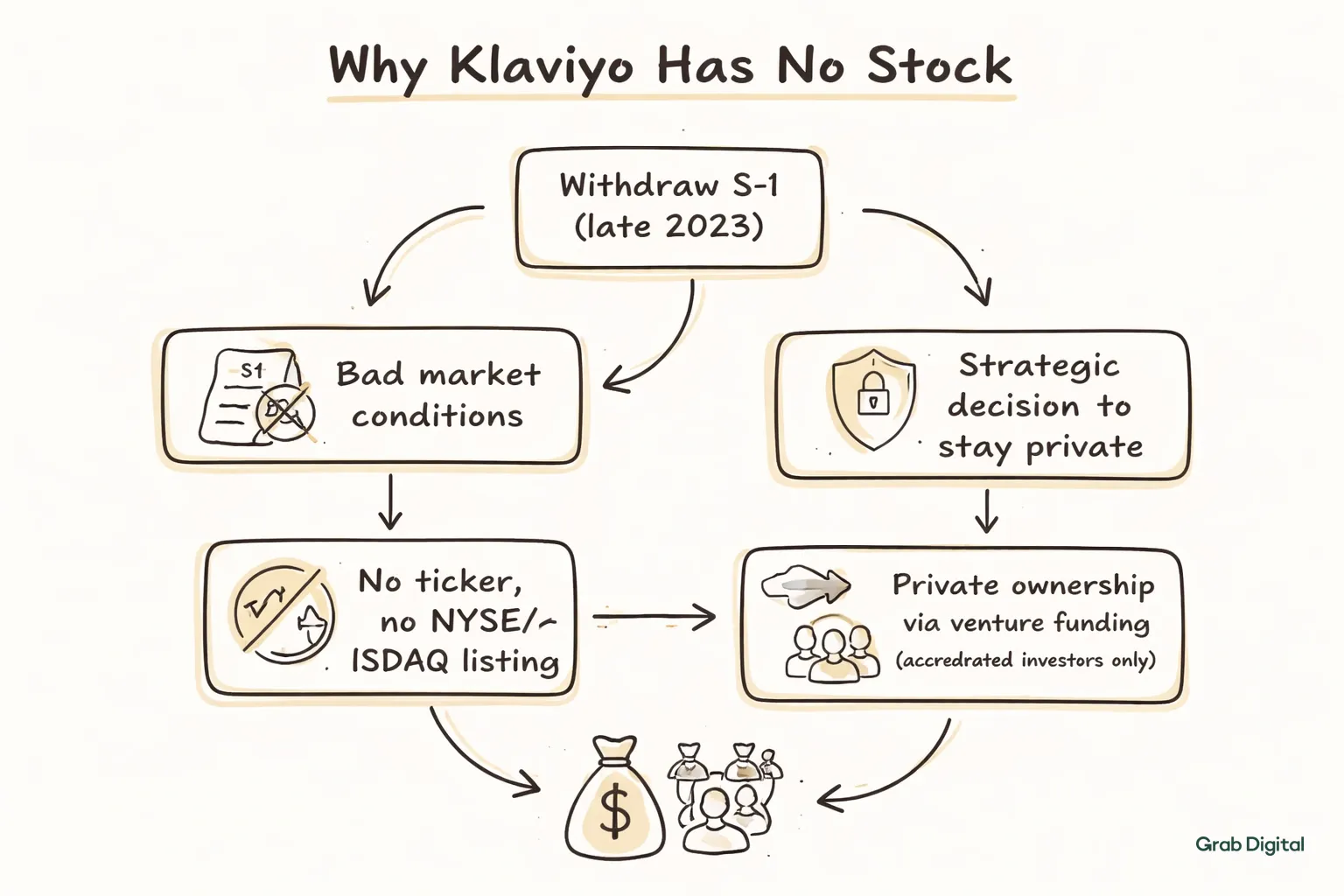

Klaviyo withdrew its S-1 in late 2023. Official reason: bad market conditions and strategic reasons to stay private. Translation: they didn't want to accept a crushed valuation. No KVYO ticker. No NYSE or NASDAQ listing.

Private companies don't list on exchanges. You can't buy Klaviyo on Robinhood, Fidelity, or Schwab. Shareholder composition stays controlled through private funding rounds no open market transactions allowed.

That hasn't changed through May 2026. No second IPO attempt. Klaviyo operates as a venture-backed private company, with ownership limited to accredited investors, institutional funds, and employees with vested options.

Actually, for DTC brands using Klaviyo as a platform, private status is probably good news. No quarterly earnings pressure forcing short-term metric chasing over customer success. If you're working with a Klaviyo agency like ours, platform continuity beats stock ticker drama.

What's Klaviyo Actually Worth?

Last disclosed valuation: $9.5 billion from the 2021 Series D. Private valuations only update when new funding happens or secondary trades leak to media. Without SEC filings, current enterprise value is guesswork.

Private market multiples got destroyed between 2021 and 2024. SaaS revenue multiples compressed 40-60% across the board. Klaviyo's paper valuation almost certainly dropped even without announcement.

Platforms like Forge Global and EquityZen occasionally facilitate private share trades for late-stage companies. These deals happen between accredited investors and existing shareholders wanting liquidity. Volume is minimal. Pricing is negotiated case-by-case.

There's no real secondary market for Klaviyo shares as of May 2026. Sporadic trades might happen through broker-dealer networks for high-net-worth clients, but that's not accessible to retail investors and doesn't reflect genuine market depth. Without exchange trading, price discovery is opaque.

Private Status: What It Means for Users

Platform risk works differently for public versus private vendors. Public companies deal with regulatory scrutiny and shareholder accountability that private firms skip. Klaviyo makes decisions without quarterly earnings calls pushing Wall Street optics over customer needs.

That freedom let them invest in CDP features, SMS expansion, and advanced segmentation without justifying burn rate to public investors. Platform probably evolved faster without analyst expectations.

Tradeoff: way less transparency. You can't pull 10-K filings to check revenue growth, churn, or cash runway. Assessing stability gets harder when financial health stays hidden.

For brands with real revenue flowing through email, that's a problem. We tell clients to diversify so no platform controls more than 40% of attributable revenue. Even working with DTC email agencies, keeping owned customer data outside Klaviyo protects optionality.

Book a free consultation to audit your email setup and find dependency risks that could hurt revenue if platform dynamics shift.

Secondary Markets (Accredited Only)

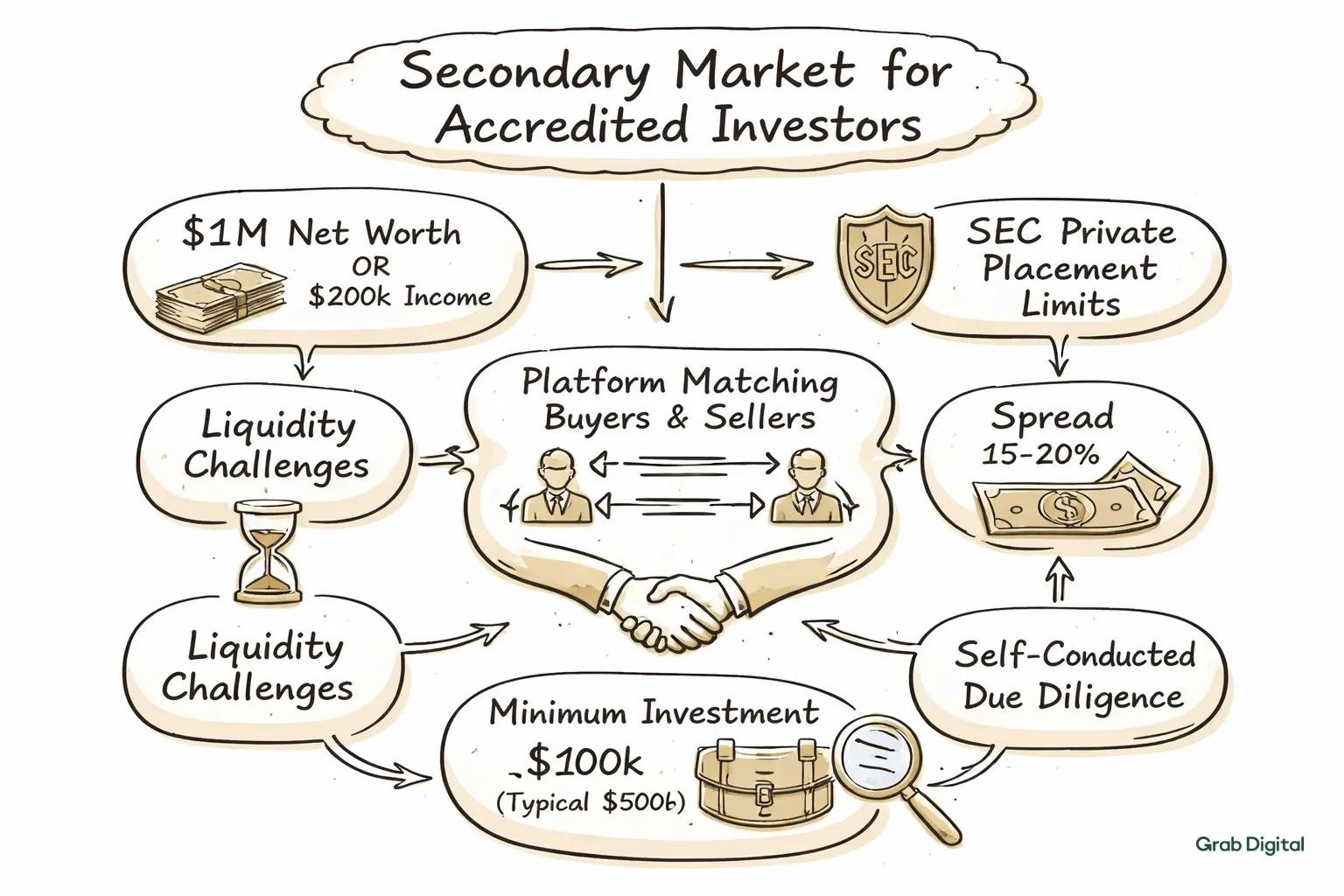

Accredited status means $1 million net worth excluding your house, or $200,000 annual income. SEC limit on who can do private placement deals for companies like Klaviyo.

Secondary platforms match qualified buyers with existing shareholders wanting liquidity. Bilateral transactions with negotiated pricing. Minimums start around $100,000 real positions need $500,000.

Liquidity is garbage. Public stocks trade continuously. Secondary private deals depend on matching buyer interest with seller willingness. Months between lots. Spreads hit 15-20%.

Due diligence is entirely on you. No analyst coverage. Projections from company materials that aren't audit-grade. Valuation from multiples applied to estimates, not audited numbers.

Works for sophisticated investors with long horizons. For retail wanting SaaS exposure, public options like Shopify offer actual liquidity.

Should You Care About Stock Status?

Functionality first. Ticker doesn't change deliverability, automation, or segmentation features driving revenue.

But ownership shapes strategy. Private companies invest in R&D without quarterly judgment. Public companies monetize users faster through price hikes and margin expansion. Klaviyo private potentially means more predictable pricing for mid-market DTC.

Acquisition risk differs too. Private Klaviyo gets acquired by Salesforce, Adobe, or HubSpot without shareholder votes. Public companies face proxy battles and regulatory reviews. Ownership shifting without customer input creates uncertainty.

Brands at $1M-$10M? These dynamics matter less than execution. Does your email automation drive 25-35% of revenue with solid attribution? Below that, ownership structure won't fix what's broken.

We see brands obsessing over Klaviyo's corporate structure while flows stay broken and campaigns fire inconsistently. Backwards approach. Build infrastructure that works regardless of vendor.

Public Alternatives

Want transparent financials? Public options exist. HubSpot (HUBS) does marketing automation including email B2B lean, not DTC focus. Salesforce (CRM) has Marketing Cloud at enterprise pricing.

Shopify (SHOP) competes with native email integrated into their commerce platform. Simpler for Shopify brands, but lacks Klaviyo's segmentation depth and personalization.

Adobe (ADBE) runs Marketo and Campaign for enterprise. Oracle (ORCL) has Eloqua and Responsys. Neither fits DTC brands under $10M too complex, too expensive.

Mailchimp (Intuit, INTU) serves small business but misses Klaviyo's ecommerce features. ActiveCampaign stays private. Constant Contact targets solopreneurs.

No public company matches Klaviyo's ecommerce positioning. If stock ownership matters more than fit, you sacrifice DTC-specific features that actually drive revenue.

Tracking Klaviyo Without a Ticker

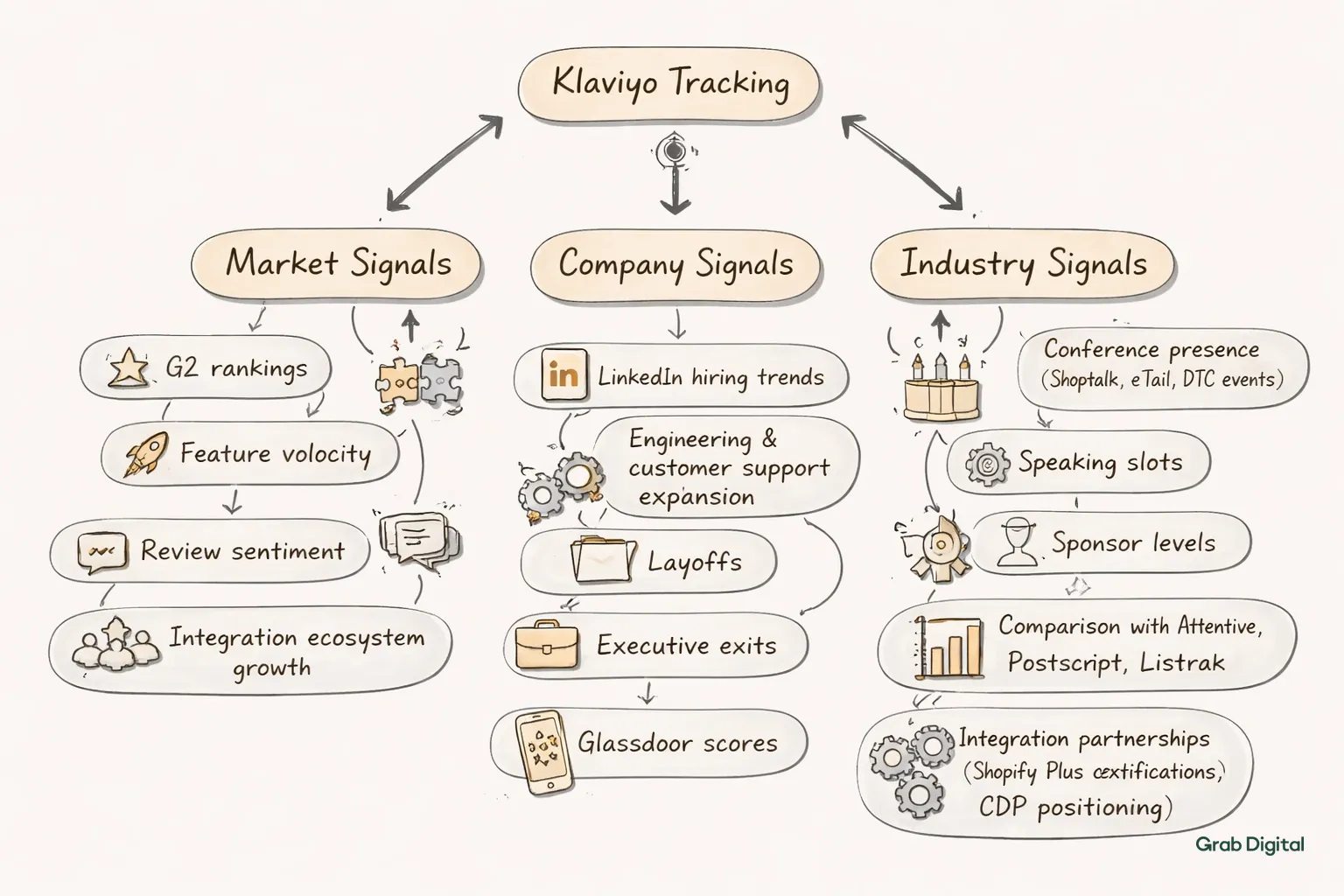

G2 rankings. Feature velocity. Review sentiment. Integration ecosystem growth. Better signals than share price.

Watch LinkedIn hiring. Engineering and CS expansion suggests growth. Layoffs or executive exits signal trouble. Glassdoor scores hint at culture affecting product quality.

Conference presence tells you something. Shoptalk, eTail, DTC events showing up matters. Speaking slots and sponsor levels indicate market commitment. Compare against Attentive, Postscript, Listrak.

Integration partnerships show direction. Shopify Plus certifications, SMS expansion, CDP positioning follow the investment. User conference roadmaps preview 12-18 months.

For lock-in risk, these signals beat stock price. Thriving private beats struggling public, ticker or not. Question is whether Klaviyo keeps shipping features solving your email revenue problems.

IPO Odds

IPO market improved through 2025. Rates stabilized, SaaS valuations recovered from 2022-2023 lows. Companies with solid unit economics went public again. Whether Klaviyo joins depends on strategy, not timing.

Founders and early investors need exits eventually. Fourteen years in, cap table has investors wanting liquidity. Secondaries help but don't match IPO scale. Pressure accumulates.

Private equity offers another path. Vista, Thoma Bravo acquire profitable SaaS regularly. Salesforce or Adobe might pay premium for Klaviyo as strategic add.

Market position matters. Maintain leadership in ecommerce email, independence makes sense. Lose ground to Shopify native tools or emerging AI platforms, selling sooner wins.

No credible IPO timeline leaked as of May 2026. No refilled S-1. Assume private through 2026 unless Bloomberg or WSJ says otherwise.

Email Marketing Exposure Without Klaviyo Stock

Want equity exposure to email growth? Look at public companies in the space. Salesforce: ~15% of revenue from Marketing Cloud. HubSpot: 40% from marketing hub with email core.

Shopify benefits from ecommerce growth driving email volume regardless of which tool brands use. More GMV correlates with more sends at scale.

Adobe Experience Cloud competes with Klaviyo at enterprise. Strong Adobe earnings signal healthy martech budgets lifting everyone.

ETFs like XSW or SKYY give diversified SaaS exposure without single-stock risk. Not pure email marketing exposure, but you avoid picking wrong winners.

For DTC brands, building enterprise value in your own business beats speculative SaaS bets. Scale past $1M with good margins, optimize email attribution, put excess cash in index funds.

What Actually Matters

Klaviyo stock availability doesn't touch your Q3 numbers. Public or private matters less than welcome series conversion, cart recovery hitting 8-12%, campaign calendar with actual strategy.

Audit performance before worrying about vendor financials. Pull 90 days of Klaviyo attribution. Email revenue as percentage of total. Under 25% means execution problems ownership structure won't solve.

Usual suspects: incomplete flows, garbage segmentation, batch-and-blast laziness, deliverability neglect. These cost 10-15 points of contribution regardless of platform.

We've fixed dozens of broken email programs stuck at 12-18% attribution. Never involves switching platforms. Takes strategy, copy, execution consistency, watching core metrics.

Underperforming email is an operational problem, not a vendor problem. Fix fundamentals. Then optimize platform leverage.

Quick Answers

Robinhood or Fidelity access?

No. Private as of May 2026. Retail accounts can't touch private equity. Accredited investors only through secondary platforms, $100K+ minimums.

Why'd they cancel?

Market conditions cratered SaaS valuations 40-60% in 2022-2023. Staying private beat accepting compressed multiples.

Going public eventually?

No timeline announced. Could IPO when conditions improve, take PE money, get acquired, or stay private indefinitely. Depends on shareholders and competition.

Private = risky for users?

Not directly. Private gives flexibility without quarterly pressure but hides financials. Real risk: product quality, retention, competitive position. Diversify channels to reduce vendor dependence.

Public competitors?

No direct equivalent. HubSpot (HUBS) and Salesforce (CRM) do email but target different markets. Shopify (SHOP) has native tools. Mailchimp (INTU) serves smaller accounts without Klaviyo's depth.

Switch based on stock status?

Bad idea. Pick on functionality, integration, pricing, support. If Klaviyo works and drives attribution, ticker availability shouldn't matter for operational decisions.

Klaviyo isn't publicly traded. You can't buy shares anywhere as of May 2026. The company pulled its IPO filing in 2023 and stayed private which means regular investors are locked out.

This catches a lot of DTC brands off guard. September 2023 had genuine IPO buzz. If you're wondering whether this matters for platform evaluation or investment exposure, here's the situation: why they pulled back, what the valuation looks like now, and whether secondary markets are even a real option.

Why There's No Klaviyo Stock

Klaviyo withdrew its S-1 in late 2023. Official reason: bad market conditions and strategic reasons to stay private. Translation: they didn't want to accept a crushed valuation. No KVYO ticker. No NYSE or NASDAQ listing.

Private companies don't list on exchanges. You can't buy Klaviyo on Robinhood, Fidelity, or Schwab. Shareholder composition stays controlled through private funding rounds no open market transactions allowed.

That hasn't changed through May 2026. No second IPO attempt. Klaviyo operates as a venture-backed private company, with ownership limited to accredited investors, institutional funds, and employees with vested options.

Actually, for DTC brands using Klaviyo as a platform, private status is probably good news. No quarterly earnings pressure forcing short-term metric chasing over customer success. If you're working with a Klaviyo agency like ours, platform continuity beats stock ticker drama.

What's Klaviyo Actually Worth?

Last disclosed valuation: $9.5 billion from the 2021 Series D. Private valuations only update when new funding happens or secondary trades leak to media. Without SEC filings, current enterprise value is guesswork.

Private market multiples got destroyed between 2021 and 2024. SaaS revenue multiples compressed 40-60% across the board. Klaviyo's paper valuation almost certainly dropped even without announcement.

Platforms like Forge Global and EquityZen occasionally facilitate private share trades for late-stage companies. These deals happen between accredited investors and existing shareholders wanting liquidity. Volume is minimal. Pricing is negotiated case-by-case.

There's no real secondary market for Klaviyo shares as of May 2026. Sporadic trades might happen through broker-dealer networks for high-net-worth clients, but that's not accessible to retail investors and doesn't reflect genuine market depth. Without exchange trading, price discovery is opaque.

Private Status: What It Means for Users

Platform risk works differently for public versus private vendors. Public companies deal with regulatory scrutiny and shareholder accountability that private firms skip. Klaviyo makes decisions without quarterly earnings calls pushing Wall Street optics over customer needs.

That freedom let them invest in CDP features, SMS expansion, and advanced segmentation without justifying burn rate to public investors. Platform probably evolved faster without analyst expectations.

Tradeoff: way less transparency. You can't pull 10-K filings to check revenue growth, churn, or cash runway. Assessing stability gets harder when financial health stays hidden.

For brands with real revenue flowing through email, that's a problem. We tell clients to diversify so no platform controls more than 40% of attributable revenue. Even working with DTC email agencies, keeping owned customer data outside Klaviyo protects optionality.

Book a free consultation to audit your email setup and find dependency risks that could hurt revenue if platform dynamics shift.

Secondary Markets (Accredited Only)

Accredited status means $1 million net worth excluding your house, or $200,000 annual income. SEC limit on who can do private placement deals for companies like Klaviyo.

Secondary platforms match qualified buyers with existing shareholders wanting liquidity. Bilateral transactions with negotiated pricing. Minimums start around $100,000 real positions need $500,000.

Liquidity is garbage. Public stocks trade continuously. Secondary private deals depend on matching buyer interest with seller willingness. Months between lots. Spreads hit 15-20%.

Due diligence is entirely on you. No analyst coverage. Projections from company materials that aren't audit-grade. Valuation from multiples applied to estimates, not audited numbers.

Works for sophisticated investors with long horizons. For retail wanting SaaS exposure, public options like Shopify offer actual liquidity.

Should You Care About Stock Status?

Functionality first. Ticker doesn't change deliverability, automation, or segmentation features driving revenue.

But ownership shapes strategy. Private companies invest in R&D without quarterly judgment. Public companies monetize users faster through price hikes and margin expansion. Klaviyo private potentially means more predictable pricing for mid-market DTC.

Acquisition risk differs too. Private Klaviyo gets acquired by Salesforce, Adobe, or HubSpot without shareholder votes. Public companies face proxy battles and regulatory reviews. Ownership shifting without customer input creates uncertainty.

Brands at $1M-$10M? These dynamics matter less than execution. Does your email automation drive 25-35% of revenue with solid attribution? Below that, ownership structure won't fix what's broken.

We see brands obsessing over Klaviyo's corporate structure while flows stay broken and campaigns fire inconsistently. Backwards approach. Build infrastructure that works regardless of vendor.

Public Alternatives

Want transparent financials? Public options exist. HubSpot (HUBS) does marketing automation including email B2B lean, not DTC focus. Salesforce (CRM) has Marketing Cloud at enterprise pricing.

Shopify (SHOP) competes with native email integrated into their commerce platform. Simpler for Shopify brands, but lacks Klaviyo's segmentation depth and personalization.

Adobe (ADBE) runs Marketo and Campaign for enterprise. Oracle (ORCL) has Eloqua and Responsys. Neither fits DTC brands under $10M too complex, too expensive.

Mailchimp (Intuit, INTU) serves small business but misses Klaviyo's ecommerce features. ActiveCampaign stays private. Constant Contact targets solopreneurs.

No public company matches Klaviyo's ecommerce positioning. If stock ownership matters more than fit, you sacrifice DTC-specific features that actually drive revenue.

Tracking Klaviyo Without a Ticker

G2 rankings. Feature velocity. Review sentiment. Integration ecosystem growth. Better signals than share price.

Watch LinkedIn hiring. Engineering and CS expansion suggests growth. Layoffs or executive exits signal trouble. Glassdoor scores hint at culture affecting product quality.

Conference presence tells you something. Shoptalk, eTail, DTC events showing up matters. Speaking slots and sponsor levels indicate market commitment. Compare against Attentive, Postscript, Listrak.

Integration partnerships show direction. Shopify Plus certifications, SMS expansion, CDP positioning follow the investment. User conference roadmaps preview 12-18 months.

For lock-in risk, these signals beat stock price. Thriving private beats struggling public, ticker or not. Question is whether Klaviyo keeps shipping features solving your email revenue problems.

IPO Odds

IPO market improved through 2025. Rates stabilized, SaaS valuations recovered from 2022-2023 lows. Companies with solid unit economics went public again. Whether Klaviyo joins depends on strategy, not timing.

Founders and early investors need exits eventually. Fourteen years in, cap table has investors wanting liquidity. Secondaries help but don't match IPO scale. Pressure accumulates.

Private equity offers another path. Vista, Thoma Bravo acquire profitable SaaS regularly. Salesforce or Adobe might pay premium for Klaviyo as strategic add.

Market position matters. Maintain leadership in ecommerce email, independence makes sense. Lose ground to Shopify native tools or emerging AI platforms, selling sooner wins.

No credible IPO timeline leaked as of May 2026. No refilled S-1. Assume private through 2026 unless Bloomberg or WSJ says otherwise.

Email Marketing Exposure Without Klaviyo Stock

Want equity exposure to email growth? Look at public companies in the space. Salesforce: ~15% of revenue from Marketing Cloud. HubSpot: 40% from marketing hub with email core.

Shopify benefits from ecommerce growth driving email volume regardless of which tool brands use. More GMV correlates with more sends at scale.

Adobe Experience Cloud competes with Klaviyo at enterprise. Strong Adobe earnings signal healthy martech budgets lifting everyone.

ETFs like XSW or SKYY give diversified SaaS exposure without single-stock risk. Not pure email marketing exposure, but you avoid picking wrong winners.

For DTC brands, building enterprise value in your own business beats speculative SaaS bets. Scale past $1M with good margins, optimize email attribution, put excess cash in index funds.

What Actually Matters

Klaviyo stock availability doesn't touch your Q3 numbers. Public or private matters less than welcome series conversion, cart recovery hitting 8-12%, campaign calendar with actual strategy.

Audit performance before worrying about vendor financials. Pull 90 days of Klaviyo attribution. Email revenue as percentage of total. Under 25% means execution problems ownership structure won't solve.

Usual suspects: incomplete flows, garbage segmentation, batch-and-blast laziness, deliverability neglect. These cost 10-15 points of contribution regardless of platform.

We've fixed dozens of broken email programs stuck at 12-18% attribution. Never involves switching platforms. Takes strategy, copy, execution consistency, watching core metrics.

Underperforming email is an operational problem, not a vendor problem. Fix fundamentals. Then optimize platform leverage.

Quick Answers

Robinhood or Fidelity access?

No. Private as of May 2026. Retail accounts can't touch private equity. Accredited investors only through secondary platforms, $100K+ minimums.

Why'd they cancel?

Market conditions cratered SaaS valuations 40-60% in 2022-2023. Staying private beat accepting compressed multiples.

Going public eventually?

No timeline announced. Could IPO when conditions improve, take PE money, get acquired, or stay private indefinitely. Depends on shareholders and competition.

Private = risky for users?

Not directly. Private gives flexibility without quarterly pressure but hides financials. Real risk: product quality, retention, competitive position. Diversify channels to reduce vendor dependence.

Public competitors?

No direct equivalent. HubSpot (HUBS) and Salesforce (CRM) do email but target different markets. Shopify (SHOP) has native tools. Mailchimp (INTU) serves smaller accounts without Klaviyo's depth.

Switch based on stock status?

Bad idea. Pick on functionality, integration, pricing, support. If Klaviyo works and drives attribution, ticker availability shouldn't matter for operational decisions.

Find out exactly what your email channel is leaving on the table.

Email Marketing for Scaling DTC Brands