Summary

Klaviyo Stock 2026: Private Company Status Explained

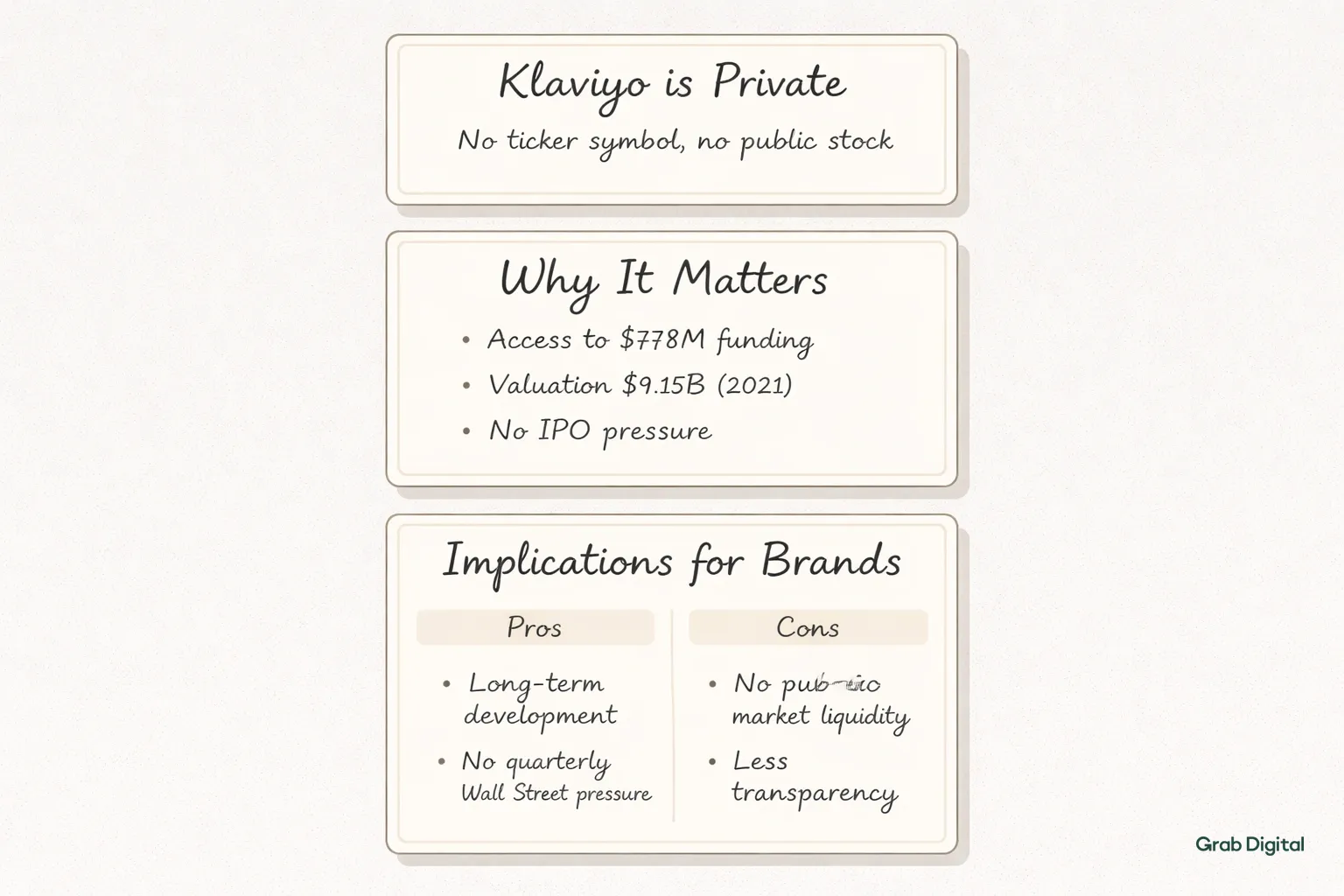

Klaviyo isn't a stock you can buy. As of May 2026, the company is still private no ticker, no public shares, no way in for regular investors. If you're here hoping to invest, you're mostly out of luck unless you have venture connections or secondary market access.

That's annoying, because Klaviyo has become the email platform for DTC brands. It's baked into how thousands of companies talk to customers. Understanding who owns it, and whether that might change, matters if you're building on their infrastructure.

Is Klaviyo Publicly Traded?

Nope. No ticker symbol. No stock.

Klaviyo has raised over $778 million from venture firms Summit Partners, Accel, Shopify. Their 2021 Series D valued them at $9.15 billion, which sounds impressive but private valuations are negotiated numbers, not market prices. What matters more is that Klaviyo has enough capital to operate without sprinting toward an IPO.

For brands, this cuts both ways. Private companies can invest in long-term development without explaining quarterly misses to Wall Street. They're not forced to cut costs or raise prices to hit short-term numbers. But you also don't see their financials. Revenue, churn, burn rate all hidden.

If you're evaluating Klaviyo as your email platform, private status shouldn't disqualify them. The investors are legitimate. The market position is strong. Most successful software companies stay private for years. Some never go public at all.

Why People Search "Klaviyo Stock"

Three groups end up here. Investors wanting to buy shares. Brand owners checking if the platform will survive. Finance people tracking where martech is headed.

Investors see Klaviyo's grip on DTC email marketing and want a piece. The platform is sticky once brands build flows and lists, switching hurts. The Shopify integration creates a real moat. If Klaviyo goes public, early investors could see real returns.

Brand owners are doing homework. Migrating email platforms is expensive and risky. You want confidence your provider will exist in five years, keep shipping features, not double your rates overnight. Private companies don't publish reports, so you're reading between the lines.

Finance people track Klaviyo because it reflects bigger shifts: email's durability, the move toward owned channels, first-party data value. When clients book consultations with us, these trends come up constantly.

Klaviyo's IPO Possibilities

Klaviyo has followed the standard venture path: seed rounds, Series A through D, growth without immediate profitability pressure. Their 2021 funding set up an eventual public offering, but no announcement yet.

The IPO window got ugly in 2022. Higher rates crushed tech valuations. Investors pulled back. By mid-2026 things have improved, but public markets remain selective. They want profitable companies with clean growth stories.

Klaviyo looks IPO-ready on fundamentals. Over 130,000 brands. Billions of monthly customer interactions. Revenue likely above $500 million annually based on public comments about growth, though exact numbers stay private.

Three things could push an IPO: public markets stabilizing with appetite for profitable software, competitive pressure from Mailchimp or Salesforce forcing a move, early investors wanting liquidity after years of holding shares.

Going public would mean transparency. Quarterly filings reveal everything revenue, customer counts, churn. You'd see how the business actually works. But public companies also face different pressures. Sometimes quarterly focus helps. Sometimes it pushes short-term decisions.

What Private Ownership Means for Your Brand

Using a private platform affects your email strategy.

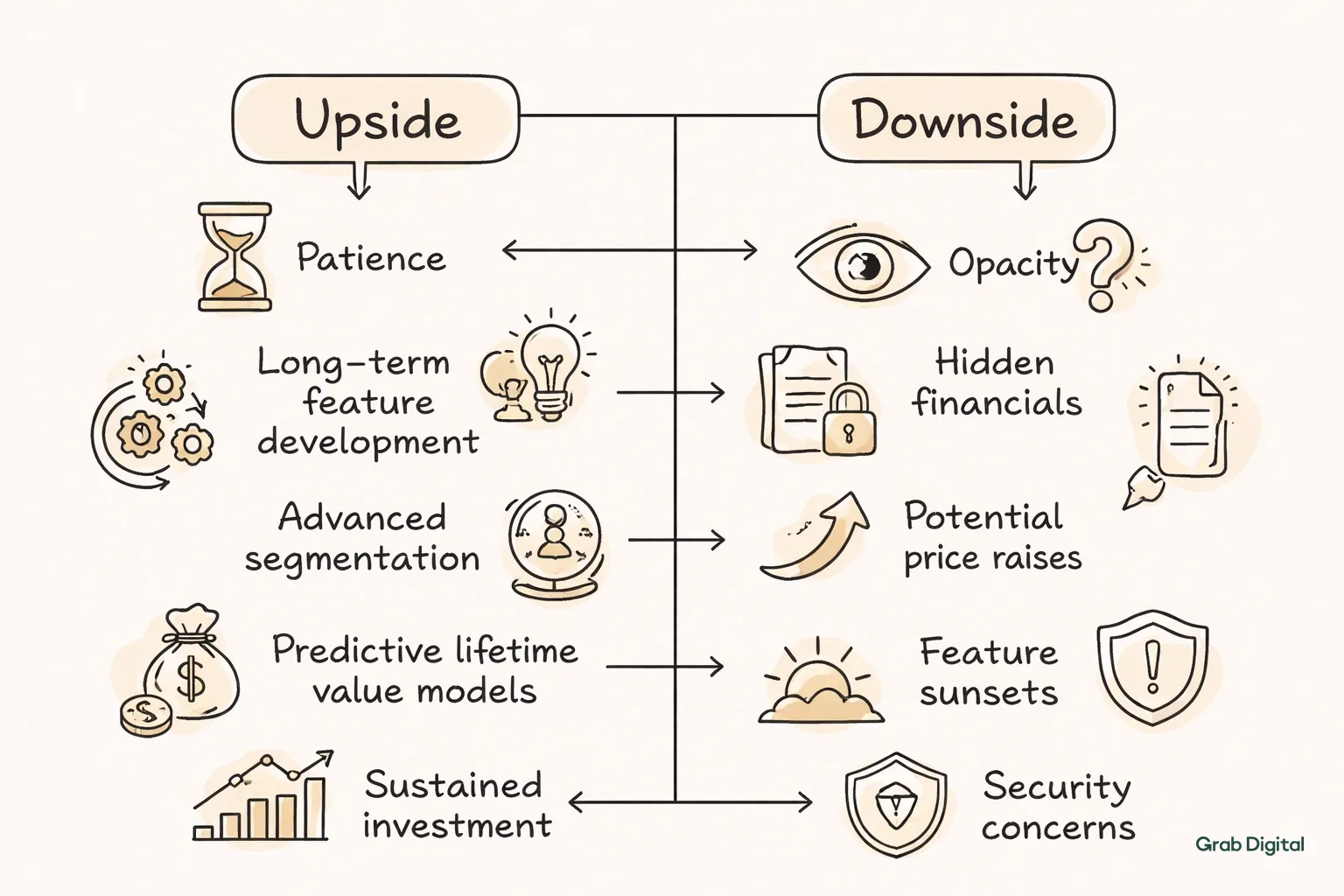

The upside: patience. Klaviyo can build features that take years without justifying them to shareholders every quarter. Their abandoned cart flows, predictive lifetime value models, and advanced segmentation) needed sustained investment. A public company might ship faster but cut corners to hit deadlines.

The downside: opacity. You can't see Klaviyo's financial position. Burn rate, long-term viability all hidden. Private companies can pivot strategy, raise prices, sunset features without explanation. Security breaches and leadership drama stay under wraps.

Here's my practical advice: diversify. Don't bet your entire customer communication strategy on one platform. Keep email list backups. Document your flows. Own your data outside Klaviyo. This matters regardless of who owns the company.

Klaviyo's investors want them to succeed, which aligns with your interest in stability. Their customer base and revenue suggest they're not disappearing. But you're trusting management without full visibility.

Investing in Email Marketing Without Klaviyo Stock

Can't buy Klaviyo directly. But you can invest in the same trends through public companies.

Shopify (SHOP) owns a Klaviyo stake and is their biggest integration partner. When Shopify merchants grow, Klaviyo benefits.

Salesforce (CRM) owns Marketing Cloud, which competes for enterprise customers. Their earnings show marketing automation spending trends.

HubSpot (HUBS) competes in email with a broader inbound platform. Their numbers reveal how brands split budgets across channels.

Intuit (INTU) bought Mailchimp for $12 billion in 2021. That acquisition validated email marketing as a real category. Intuit investors get small business marketing exposure.

None of these track Klaviyo perfectly. But they capture related trends. DTC growth, first-party data demand, owned channel marketing all lift these stocks.

How Private Ownership Shapes Product

Being private lets Klaviyo invest in projects without immediate payoffs. No quarterly earnings calls means they can build SMS, customer data platforms, AI personalization over years.

The eight core email flows show this. Welcome series, browse abandonment, winback automation these took sustained development. Rushing would have hurt them.

Venture investors care about market dominance, not quarterly profit. That alignment lets Klaviyo prioritize retention and quality over squeezing customers. The platform is more stable for it.

Public competitors face different math. Infrastructure upgrades get delayed. Features ship incomplete. Prices rise to hit targets. Those decisions help stock prices, sometimes hurt customers.

Trade-off: accountability. Public companies must explain themselves. Private companies pivot quickly but communicate less. You're trusting judgment without the full picture.

Reading Klaviyo Without Financial Statements

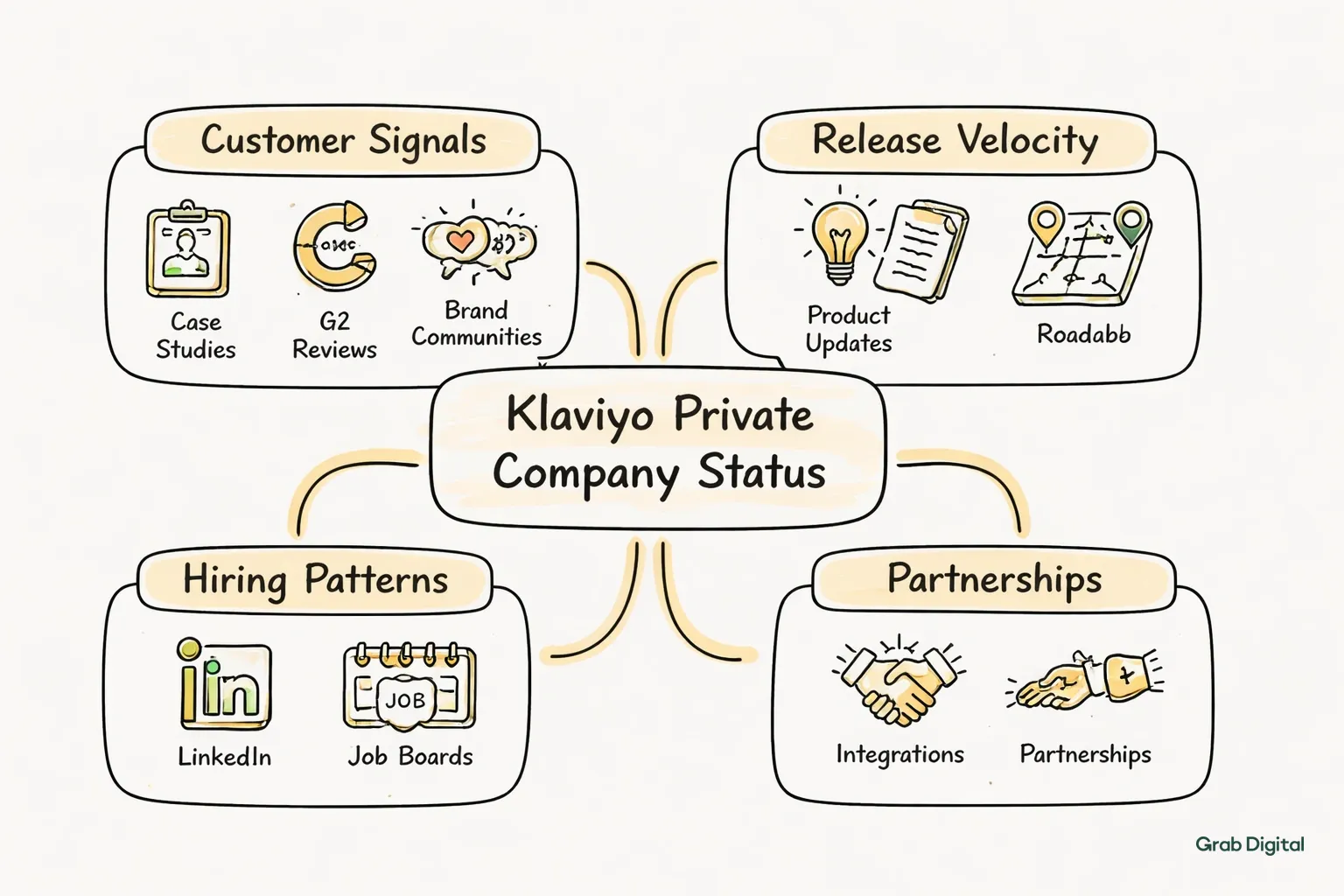

You can assess Klaviyo's health through public signals. Financial reports aren't the only way.

Customer signals: Case studies, G2 reviews, brand communities. When DTC brands choose Klaviyo and stay, that's product-market fit. High churn would be a red flag.

Release velocity: Klaviyo ships regular updates. If releases slow or roadmap items disappear, something's wrong.

Hiring patterns: LinkedIn and job boards show expansion or contraction. Growing teams mean confidence. Hiring freezes signal trouble.

Partnerships: New integrations expand reach. Partnership losses weaken position.

Pricing stability: Klaviyo's pricing has stayed consistent, scaling with contacts. Sudden increases without new features might indicate margin pressure.

Not perfect signals. But enough to make informed decisions. A good email agency can help you read these for your situation.

What Changes If Klaviyo Goes Public

An IPO would shift things. More transparency, but also more pressure on product and pricing.

Financial disclosure: Customer counts, revenue per customer, churn, margins. You'd benchmark yourself against others.

Earnings calls: Management explains strategy publicly. You'd hear priorities and competitive positioning.

Pricing pressure: Shareholders want consistent growth. Price increases and new fees often follow. Free features might get paywalled.

Roadmap transparency: Could improve or decline. Some companies communicate more publicly. Others get secretive to hide from competitors.

Support: Efficiency pressure might mean longer wait times or tiered support.

Development speed: Depends on what Klaviyo does with public capital. Accelerate with new funding? Slow down under profit pressure?

If you use Klaviyo, consider locking in multi-year contracts before any IPO. Document features you depend on. Keep alternatives warm.

Building Strategy That Outlasts Any Platform

Smart brands don't tie their email program to one company's fate. Your email strategy should survive acquisitions, IPOs, pivots.

Own your data. Export lists, purchase history, engagement metrics. Store backups outside Klaviyo in portable formats.

Document flows. Write specs any platform could replicate. Don't just build in Klaviyo document the logic.

Test alternatives yearly. You don't need to switch. But know what migration costs. Run small tests on competitors.

Diversify channels. SMS, push, direct mail. Reduces email dependence and protects against deliverability problems or outages.

Build expertise, not just platform knowledge. Segmentation, personalization, lifecycle marketing these transfer across tools. Invest through hiring or an agency partnership.

Not about leaving Klaviyo. About using platforms strategically while keeping options open.

FAQ

Can I buy Klaviyo stock in 2026? No. Private company. Only accredited investors with secondary market access can get shares, and those opportunities are thin.

Will Klaviyo go public soon? Nothing announced. Valuation and position suggest they could, but timing depends on markets and management. Watch official channels.

Should I worry about using a private platform? Depends. Klaviyo's funding and customer base suggest stability. Focus on product quality and fit. Ownership structure matters less than whether the tool works.

What happens to my data if Klaviyo gets acquired? Your data stays yours. Service agreement terms survive acquisitions. Keep backups anyway. Monitor agreement changes after any corporate event.

How do I invest in email marketing without Klaviyo stock? Shopify, Salesforce, HubSpot, Intuit (Mailchimp's owner) all give exposure to email trends. Cloud software ETFs work too.

Does private ownership affect product development? Usually yes longer investment horizon without quarterly pressure. Klaviyo can build complex features without immediate payoffs. That often helps customers, but you lose financial visibility.

Klaviyo isn't a stock you can buy. As of May 2026, the company is still private no ticker, no public shares, no way in for regular investors. If you're here hoping to invest, you're mostly out of luck unless you have venture connections or secondary market access.

That's annoying, because Klaviyo has become the email platform for DTC brands. It's baked into how thousands of companies talk to customers. Understanding who owns it, and whether that might change, matters if you're building on their infrastructure.

Is Klaviyo Publicly Traded?

Nope. No ticker symbol. No stock.

Klaviyo has raised over $778 million from venture firms Summit Partners, Accel, Shopify. Their 2021 Series D valued them at $9.15 billion, which sounds impressive but private valuations are negotiated numbers, not market prices. What matters more is that Klaviyo has enough capital to operate without sprinting toward an IPO.

For brands, this cuts both ways. Private companies can invest in long-term development without explaining quarterly misses to Wall Street. They're not forced to cut costs or raise prices to hit short-term numbers. But you also don't see their financials. Revenue, churn, burn rate all hidden.

If you're evaluating Klaviyo as your email platform, private status shouldn't disqualify them. The investors are legitimate. The market position is strong. Most successful software companies stay private for years. Some never go public at all.

Why People Search "Klaviyo Stock"

Three groups end up here. Investors wanting to buy shares. Brand owners checking if the platform will survive. Finance people tracking where martech is headed.

Investors see Klaviyo's grip on DTC email marketing and want a piece. The platform is sticky once brands build flows and lists, switching hurts. The Shopify integration creates a real moat. If Klaviyo goes public, early investors could see real returns.

Brand owners are doing homework. Migrating email platforms is expensive and risky. You want confidence your provider will exist in five years, keep shipping features, not double your rates overnight. Private companies don't publish reports, so you're reading between the lines.

Finance people track Klaviyo because it reflects bigger shifts: email's durability, the move toward owned channels, first-party data value. When clients book consultations with us, these trends come up constantly.

Klaviyo's IPO Possibilities

Klaviyo has followed the standard venture path: seed rounds, Series A through D, growth without immediate profitability pressure. Their 2021 funding set up an eventual public offering, but no announcement yet.

The IPO window got ugly in 2022. Higher rates crushed tech valuations. Investors pulled back. By mid-2026 things have improved, but public markets remain selective. They want profitable companies with clean growth stories.

Klaviyo looks IPO-ready on fundamentals. Over 130,000 brands. Billions of monthly customer interactions. Revenue likely above $500 million annually based on public comments about growth, though exact numbers stay private.

Three things could push an IPO: public markets stabilizing with appetite for profitable software, competitive pressure from Mailchimp or Salesforce forcing a move, early investors wanting liquidity after years of holding shares.

Going public would mean transparency. Quarterly filings reveal everything revenue, customer counts, churn. You'd see how the business actually works. But public companies also face different pressures. Sometimes quarterly focus helps. Sometimes it pushes short-term decisions.

What Private Ownership Means for Your Brand

Using a private platform affects your email strategy.

The upside: patience. Klaviyo can build features that take years without justifying them to shareholders every quarter. Their abandoned cart flows, predictive lifetime value models, and advanced segmentation) needed sustained investment. A public company might ship faster but cut corners to hit deadlines.

The downside: opacity. You can't see Klaviyo's financial position. Burn rate, long-term viability all hidden. Private companies can pivot strategy, raise prices, sunset features without explanation. Security breaches and leadership drama stay under wraps.

Here's my practical advice: diversify. Don't bet your entire customer communication strategy on one platform. Keep email list backups. Document your flows. Own your data outside Klaviyo. This matters regardless of who owns the company.

Klaviyo's investors want them to succeed, which aligns with your interest in stability. Their customer base and revenue suggest they're not disappearing. But you're trusting management without full visibility.

Investing in Email Marketing Without Klaviyo Stock

Can't buy Klaviyo directly. But you can invest in the same trends through public companies.

Shopify (SHOP) owns a Klaviyo stake and is their biggest integration partner. When Shopify merchants grow, Klaviyo benefits.

Salesforce (CRM) owns Marketing Cloud, which competes for enterprise customers. Their earnings show marketing automation spending trends.

HubSpot (HUBS) competes in email with a broader inbound platform. Their numbers reveal how brands split budgets across channels.

Intuit (INTU) bought Mailchimp for $12 billion in 2021. That acquisition validated email marketing as a real category. Intuit investors get small business marketing exposure.

None of these track Klaviyo perfectly. But they capture related trends. DTC growth, first-party data demand, owned channel marketing all lift these stocks.

How Private Ownership Shapes Product

Being private lets Klaviyo invest in projects without immediate payoffs. No quarterly earnings calls means they can build SMS, customer data platforms, AI personalization over years.

The eight core email flows show this. Welcome series, browse abandonment, winback automation these took sustained development. Rushing would have hurt them.

Venture investors care about market dominance, not quarterly profit. That alignment lets Klaviyo prioritize retention and quality over squeezing customers. The platform is more stable for it.

Public competitors face different math. Infrastructure upgrades get delayed. Features ship incomplete. Prices rise to hit targets. Those decisions help stock prices, sometimes hurt customers.

Trade-off: accountability. Public companies must explain themselves. Private companies pivot quickly but communicate less. You're trusting judgment without the full picture.

Reading Klaviyo Without Financial Statements

You can assess Klaviyo's health through public signals. Financial reports aren't the only way.

Customer signals: Case studies, G2 reviews, brand communities. When DTC brands choose Klaviyo and stay, that's product-market fit. High churn would be a red flag.

Release velocity: Klaviyo ships regular updates. If releases slow or roadmap items disappear, something's wrong.

Hiring patterns: LinkedIn and job boards show expansion or contraction. Growing teams mean confidence. Hiring freezes signal trouble.

Partnerships: New integrations expand reach. Partnership losses weaken position.

Pricing stability: Klaviyo's pricing has stayed consistent, scaling with contacts. Sudden increases without new features might indicate margin pressure.

Not perfect signals. But enough to make informed decisions. A good email agency can help you read these for your situation.

What Changes If Klaviyo Goes Public

An IPO would shift things. More transparency, but also more pressure on product and pricing.

Financial disclosure: Customer counts, revenue per customer, churn, margins. You'd benchmark yourself against others.

Earnings calls: Management explains strategy publicly. You'd hear priorities and competitive positioning.

Pricing pressure: Shareholders want consistent growth. Price increases and new fees often follow. Free features might get paywalled.

Roadmap transparency: Could improve or decline. Some companies communicate more publicly. Others get secretive to hide from competitors.

Support: Efficiency pressure might mean longer wait times or tiered support.

Development speed: Depends on what Klaviyo does with public capital. Accelerate with new funding? Slow down under profit pressure?

If you use Klaviyo, consider locking in multi-year contracts before any IPO. Document features you depend on. Keep alternatives warm.

Building Strategy That Outlasts Any Platform

Smart brands don't tie their email program to one company's fate. Your email strategy should survive acquisitions, IPOs, pivots.

Own your data. Export lists, purchase history, engagement metrics. Store backups outside Klaviyo in portable formats.

Document flows. Write specs any platform could replicate. Don't just build in Klaviyo document the logic.

Test alternatives yearly. You don't need to switch. But know what migration costs. Run small tests on competitors.

Diversify channels. SMS, push, direct mail. Reduces email dependence and protects against deliverability problems or outages.

Build expertise, not just platform knowledge. Segmentation, personalization, lifecycle marketing these transfer across tools. Invest through hiring or an agency partnership.

Not about leaving Klaviyo. About using platforms strategically while keeping options open.

FAQ

Can I buy Klaviyo stock in 2026? No. Private company. Only accredited investors with secondary market access can get shares, and those opportunities are thin.

Will Klaviyo go public soon? Nothing announced. Valuation and position suggest they could, but timing depends on markets and management. Watch official channels.

Should I worry about using a private platform? Depends. Klaviyo's funding and customer base suggest stability. Focus on product quality and fit. Ownership structure matters less than whether the tool works.

What happens to my data if Klaviyo gets acquired? Your data stays yours. Service agreement terms survive acquisitions. Keep backups anyway. Monitor agreement changes after any corporate event.

How do I invest in email marketing without Klaviyo stock? Shopify, Salesforce, HubSpot, Intuit (Mailchimp's owner) all give exposure to email trends. Cloud software ETFs work too.

Does private ownership affect product development? Usually yes longer investment horizon without quarterly pressure. Klaviyo can build complex features without immediate payoffs. That often helps customers, but you lose financial visibility.

Find out exactly what your email channel is leaving on the table.

Email Marketing for Scaling DTC Brands